Are you struggling each month to save money? Do you get to the end of the month and wonder where did all my money go? Are you living beyond your means?

If this sounds like you then you are in exactly the right place. It’s time to revisit your relationship with money. Saving money is about your mindset, financial habits, and the decisions that you make.

Saving money should not be a burden, but rather a well-planned effort.

I went through a really bad time financially and it was these lessons that changed my life. I only wish that I had learned them when I was much younger.

Go through them, apply the techniques and strategies that I’ve included, and you may just discover that you have a lot more cash available than you thought.

Ready to get started? Let’s go.

Only Buy What You Can Afford

Living within your means can be extremely challenging, but it’s a must if you want to get your finances under control.

You may think that you can’t live without that latest gadget, or whatever it is that pulls at you, but if you can’t afford it then don’t buy it. The financial difficulties that it will create will overshadow the satisfaction that you get. Plus, in most cases, it’s just an initial high followed by buyer’s remorse.

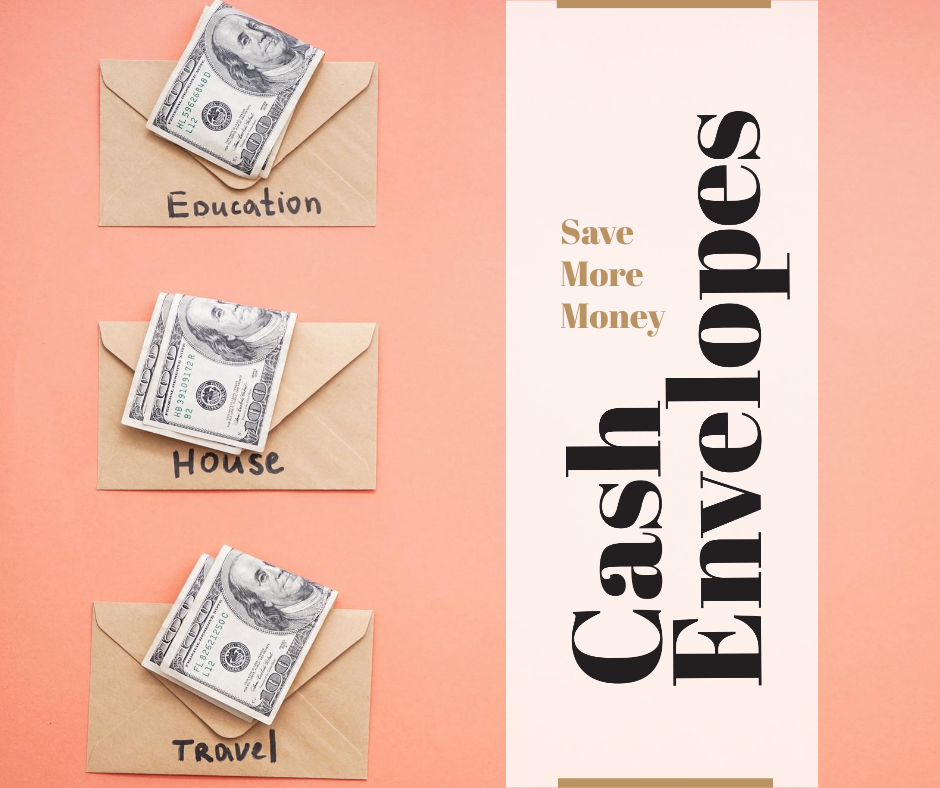

Consider using the good old fashioned cash envelope system. Make a list and categorize all of your monthly expenses. Label the envelope with the category name. Add additional categories for saving money, such as an emergency fund or saving for a holiday.

Allocate the amount of money that goes into each envelope. Then fill the envelope with the budgeted amount on payday or at the beginning of each month. Pay for everything from the envelopes. Once the envelopes are empty you have finished spending on that category for the month.

If you have money left over at the end of the month that should go into the saving envelope. Be mindful of your spending and stay focused on your savings goal. You’ll be surprised at how quickly the money will start to add up.

Know the Difference Between Needs and Wants

Needs are easy. They include anything that is required to live. Food, water, shelter, clothing are the basics. Of course, we have to add into this list electricity, phone, cable, internet, etc.

Wants, on the other hand, include all that stuff that makes you feel good.

Learn to differentiate between the two and you’ll start making decisions that will help you save money. Each time you want to buy something ask yourself, “do I need this?”. If the answer is ‘no’ walk away.

Each time you want to buy something ask yourself, “do I need this?”. If the answer is ‘no’ walk away.

kristy shaw, savings blogger

One of the things that I have found to be especially helpful is to plan ahead. Prioritize your spending. For example, if I’m going grocery shopping, I plan out my menu for the week. This way I know what I need to buy.

I also assign myself a grocery budget. I know exactly how much money I have per month towards food. This ensures that I don’t overspend.

But what if I see something really good on sale? How do I avoid impulse buying?

The truth is I don’t. That’s where what I refer to as “wiggle room” comes into play. I allow myself enough flexibility so that if I see something that I need I can buy it while taking advantage of the sale.

Just last week I was in the grocery store and the coffee that I normally buy was on sale (three for the price of two). As it’s a staple item in my home I’ve already budgeted for it at the higher cost. However, I have not budgeted to buy three packages in one week. This will push me over my budget.

So, what should I do? Should I buy the coffee while it’s on sale or wait and pay the normal price?

Obviously, I’m going to buy it on sale knowing that I will go over budget. But that’s o.k. because I look at the month as a whole. As long as I don’t go over the monthly food budget that’s fine.

And what about wants, how do I build in wants so that I don’t feel like I’m losing out on things. Again, budget for them.

Set aside a small amount of money each month for wants. That does not mean that you must spend that money every month. Put the money into an envelope labelled “wants” and if there is nothing you want this month then carry the money to the next. Now imagine if you go three months without buying anything. That means that you can buy something bigger, more expensive. Think of how good that will make you feel.

It’s not about depriving yourself but rather becoming a good money manager. Know what you need. Know what you can afford. And reward yourself with wants.

Control Your Money Rather Than Your Money Controlling You

You need to be in control of what you are spending your money on. We so often spend frivolously that we have no idea where our money goes. If I asked you right now to write down every single thing that you spent money on last month would you be able to do that? Probably not.

For the next month, I want you to record and track every single penny that you spend. Microsoft Excel is great for this or any app that allows you to build lists. You can even just write it out with pen and paper.

In the first column, I want you to describe what you bought or paid for. Let’s say you paid your mobile phone bill. Write it down. Then in the second column record the amount.

Now take a look at the type of items that are in the first column. Are there entries that can be categorized together? For example, let’s say you bought a pair of shoes and a jacket. These are two separate items bought on two separate days, but they both are clothing. So, in the third column, you would write clothing.

Go through all of the list items and divide them into categories. Some examples may be travel expenses, groceries, household payments, car-related expenses, etc.

At the end of the month add up the total amount spent on each category. You may be shocked to see where your money has gone.

How much did you actually spend on things that you don’t need? Are there categories where you can reduce costs and save money? Look at the information logically and create a plan to cut costs for the following month. Write it down.

Once you’ve done this analysis and you have identified where exactly you were overspending take that amount of money that you’ve overspent and put that directly into your savings fund.

Find Ways to Have Fun Without Spending Money

Have you ever noticed how we socialize to a large degree revolves around money? Why is that? Whose interests are we really supporting?

We all know that money doesn’t bring you happiness, but rather the life experiences that we have. It’s our family, our friendships, those special moments that make us happy. It’s the memories that we create and the bonds that we build with others.

Happiness comes from the life that you live not the possessions that you own.

kristy shaw, savings blogger

Happiness comes from the life that you live not the possessions that you own.

So, how do you have fun without spending money?

For starters, invite your friends to your home for a potluck dinner. Have everyone come with a dish to share. Make it a theme night.

Or what about a movie and popcorn night with that special someone? There’s no rule that says you have to go to the movies and spend $100 bucks for a night out. Plus, just think of how cozy staying at home can be.

Make a list of things that you enjoy doing. Are you an outdoor person? What about going camping or hiking? Maybe you’re into sports. Why not join a community sports team? Volleyball, soccer, baseball, bowling…anyone?

Or maybe you like board games. Try hosting a board game night at your house.

Whatever it is that brings you joy write it down. Ask your friends to make their own lists. Then choose an event when you want to get together. You’re all going to have fun and save money too!

A $20k Car Takes You from Point A-to-B the Same as a $5k Car

I learned this important lesson from my Economics Professor. I remember the lecture as if it was yesterday.

I’ve never understood why people buy cars they cannot afford. It just does not make economic sense.

economics professor, ccnm

He said, “I’ve never understood why people buy cars they cannot afford. It just does not make economic sense. A $20,000 car will take you from point A to point B just the same as a $5000 car will.”

He went on to talk about how the price of cars is such a wide spectrum that there is a car for every single budget. Know your numbers.

A few months prior to that lecture I had just bought a $20,000 vehicle. And exactly 2 weeks before, to the day, my best friend at University bought a $5000 car. True story. I couldn’t believe it!

In case you’re wondering how that story ended that car got me into a huge financial mess. I bought into this idea that if I had a more expensive car it would be more reliable. And it was. The car was fantastic, but it was way beyond my means. I put myself into a chokehold with my finances and I will never forget that.

Fast forward a few years to when I had lost everything. I needed a car to get around. I had $1,500 cash in my account and not a penny more. That was the budget. It took a few months of actively researching used car websites until I found my car. I called her my little red “putt-putt”.

And I must say that is the best car I ever owned. I had that car for 5 years and when I think of the amount that I spent on maintenance and repairs it was nothing. I couldn’t believe it. Boy, were my beliefs wrong.

So, I want you to think about the car that you are driving. Is it within your budget? If not, you may want to consider making a change.

Do you want to struggle every single month with a huge car payment you cannot afford as I did? Believe me, it’s not worth it.

Don’t become a prisoner of vanity or false beliefs.

kristy shaw, savings blogger

Work your numbers and figure out how much of your income per month can you realistically afford towards a car payment. Or maybe you are better off just buying a car outright like I did. Don’t become a prisoner of vanity or false beliefs. There are tons of really amazing cars out there with super low-price points. Look around and you will find your little “putt-putt” too.

Avoid Becoming House Rich Cash Poor

Let’s face it we all have to live somewhere. But I ask you is it worth it to take a huge portion of your income and put that towards house expenses at the cost of being deprived of everything else?

It’s so easy to get caught up in the excitement of buying a house, especially for first time home buyers, that you can be leading yourself right into the house poor trap.

Remember this…

A smaller house has a smaller mortgage, which means a lower monthly payment. Plus, you can pay it off faster. Would you rather be a homeowner, or someone indebted to the bank?

Moreover, let’s not forget that the cost of repairs and renovations will be lower. But most importantly is the upkeep. That includes all your utilities. Your electricity, heating, water, and insurance. All of it…lower.

Do you see where I’m going here? Are you seeing all of the money that you can save? Money for retirement, for an emergency fund, for that holiday that you’ve been dreaming about taking for the last 10 years. Finally, you can have it all.

If you’re spending more than 50% of your income on housing, then you need to downsize. The magic number is somewhere between 25% to 35%.

kristsy shaw, savings blogger

If you’re spending more than 50% of your income on housing, then you need to downsize. The magic number is somewhere between 25% to 35%.

I recommend that you get some help doing this. Talk to a Financial Advisor. Find a Real Estate agent that will help you find a home within your budget. Downsizing is very common nowadays and there are tons of professionals that know and understand how to do this the right way.

Now I often get asked the question…

What about renting? So, let me answer that here.

In some situations, I do believe that it is a good idea to rent. Maybe you need to completely cut down all of your expenses or maybe you need to save for a down payment. However, I do think that renting should be a short-term solution.

I believe strongly in the importance of building your asset portfolio and real estate should be one of those assets.

Being Frugal Does Not Mean You are Cheap

When I think of the meaning of frugal, I think of someone that is wise with their spending. Someone that is not wasteful with their money and thinks through their money decisions.

Is it really a good idea to eat out every day? Or to get your coffee fix at Starbucks? Why not take all that money spent on fast food and coffee runs daily and put it into your savings? Try putting it into a savings envelope daily and see how much you have at the end of one month, two months, and so on.

And what about all of those TV channels that you are paying for? Do you really need them all? Realistically how much TV are you watching? Try free streaming platforms online. Many TV channels now include a video library on their website that you can watch for free.

Go through all of your current spending. Everything. Are there places where you are being wasteful? Where can you cut down? Really dive deep into the decisions that you have made. Just because you have expenses locked in it does not mean they cannot be changed.

Think about your phone bill, TV, gym membership, etc. Maybe you are not using your phone enough to justify an unlimited plan. I recently got rid of my monthly plan and got the 500 minutes per month option instead. This cut my phone bill by half. I did the same with my cable plan. I was paying for two box rentals (one for the bedroom and one for the living room). I have not turned on the TV in my bedroom for over a year so why am I paying for that. And with the gym how often do you go? Is a pay-as-you-go option better than the full access membership?

Do you see where I am going here? Question each expense. Is there a way to reduce the cost? Negotiate your contracts when possible.

Then take that extra money that you save each month and put it towards your money-saving goals. For example, transfer it directly to a savings account. With some banks, you can even automate the whole process. Set and forget.

Final Thoughts

Saving money should not be a hassle. Set up systems that are easy to follow. Manage your money and let it work for you. Focus on the big picture. What do you want in life? How important is your financial freedom?

Learn to make good money decisions based on your income. Don’t live beyond your means and put yourself in a financial chokehold even if that cute little $20,000 red sports car looks good.

Be patient with your savings efforts. Build good money habits. Know your limits and buy only what you can afford. And make sure to get on top of your spending by recording and tracking. Remember we’re in this for the long haul.